Macroeconomic Impacts of US

Sanctions (2017-2019) on Iran

SHAHROKH FARDOUST

EXECUTIVE SUMMARY

This paper examines the effects of the “maximum pressure” sanctions imposed by the U.S. after it unilaterally pulled out of the Joint Comprehensive Plan of Action (JCPOA) — also known as the Iran nuclear deal — in early 2018. It shows that in the two most recent years for which macroeconomic data are available (2018 and 2019), Iran’s per capita real income fell by about 14 percent (6.8 percent a year) — more than twice the pace of decline during the pre JCPOA sanction episode (2012–2015) and substantially higher than the average drop of 3 to 4 percent a year in GDP per capita growth in countries under trade sanctions.

Moreover, during 2018-2019 (and continuing in 2020) Iran’s inflation rate nearly quadrupled from 9.6 percent to more than 40 percent a year, oil exports fell (cumulatively) by $80 billion, capital outflows continued, and the rial lost nearly 80 percent of its value against the U.S. dollar.

Preliminary calculations suggest that had Iran’s economy grown at its long-term pre-sanction rate of 4.1 percent a year, per capita real income in 2019 would have been almost 30 percent higher than its level in 2012, first year under the nuclear-related UN sanctions, rather than 13.5 percent lower.

Continuation of the “maximum pressure” strategy, combined with devastating COVID-19 pandemic-related losses, is likely to result in another 6-8 percent reduction in per capita real income in 2020, further increasing poverty and inequality and possibly creating a humanitarian crisis.

By reducing Iran’s oil exports from about 2.5 million barrels per day (mbd) to around 0.5 mbd, the US imposed sanctions seriously weakened Iran’s fiscal and balance of payments positions as a result of the sharp declines in the government’s revenues oil revenues and foreign exchange proceeds from oil exports. This has led to continuation of Iran’s high inflation rate, resulting from the expansion of the monetary base to finance the growing budget deficit, as well as a sharp devaluation of the national currency due to inappropriate exchange rate policy, significant capital outflows, stranded assets and loss of access to official foreign exchange reserves.

Had Iran undertaken serious fiscal and banking/financial reforms during 2006- 2011, however, it would have been able to reduce sanctions’ impact on its economy and population. Iran’s investment climate, undermined by serious governance issues and an unstable policy environment, also contributed to low and declining private investment, particularly in manufacturing, while the sharp decline in public investment, particularly since 2017, has shaken private sector confidence.

Even though the sanctions have forced Iran to become more self-reliant and its economy has become more diversified, the longer-term adverse economic and social impacts of sanctions are likely to be substantial. The sharp declines in real per capita has already led to a substantial erosion of living standards for the middle class and poor. The substantial drop in investment — private, public and FDI — during the past decade implies much lower output growth in coming years, resulting from the expected declines in both labor and total factor productivity growth rates.

The “maximum pressure” sanctions have undermined the ability of Iran’s public and private sectors to deal with the pandemic. The next 12 to 18 months will be particularly difficult for Iran, as on top of the sanctions and pandemic, the global recession and expected slow recovery are likely to constrain its oil and non-oil exports, and the level of official reserves is likely to continue to decline.

Policymakers hope they can reach an understanding with the U.S. if its incoming administration brings about foreign policy change, including in regard to the Middle East. Even if this scenario pans out, however, change will more likely occur gradually, rather than quickly and in a significant manner. Given the serious humanitarian crisis Iranians face, the most feasible improvements would probably involve removal of some restrictions on oil exports and international banking and allowance of financial assistance from international financial institutions for purposes related to COVID-19.

I. INTRODUCTION

This paper first examines the macroeconomic effects of the trade and financial sanctions the U.S., European Union (EU) and UN imposed prior to the JCPOA (the Iran nuclear deal). It then analyzes the effects of the “maximum pressure” sanctions the U.S. imposed after unilaterally leaving that agreement in 2018. It is based on a review of sanctions literature, estimates of changes in key Iranian macroeconomic indicators during the Sanctions I (2012- 2015) and Sanctions II (2018-2019 and continuing) periods and a comparison with the economy’s historical performance in 1995-2011. It also examines model-based, pre-sanctions, medium-term forecasts of the economy for 2012-2019, and compares the effects of sanctions on Iran with those on Russia and Venezuela, two other oil-exporting countries subjected to such measures in the same period.

II. U.S. WITHDRAWAL FROM THE JCPOA AND NEW U.S. SANCTIONS

In 2018, the Trump administration unilaterally withdrew the U.S. from the nuclear deal that had been concluded following prolonged and intensive negotiations with Iran in July 2015 by the P5+1 (the five permanent members of the UN Security Council plus Germany) and the EU, then endorsed by the UN Security Council [1]. Making good on a campaign promise, President Trump issued an executive order on 8 May 2018 announcing that the U.S. would no longer participate in the JCPOA and would reimpose the sanctions that had been lifted (or suspended) as a result of that agreement [2]. The stated reasons were that Washington believed Iran had undertaken nuclear activities that exceeded agreed limits and was accruing inappropriate benefits, and that efforts by the remaining signatories were inadequate to sustain the agreement. Iran initially asserted that it would continue to honor and implement its commitments under the deal as long as the remaining signatories did likewise and allowed it to receive anticipated benefits.

Since mid-2018, the U.S. has been pursuing a “maximum pressure” strategy, continuously expanding existing sanctions and adding numerous new ones [3]. On 6 November 2018, it re-imposed all sanctions, including secondary ones under which it penalizes third parties (firms and countries) that engage with Iran. The stated purpose is to pressure Iran to negotiate a new deal that takes into account Trump administration concerns about the JCPOA and goes beyond the nuclear program to encompass a wholesale change in Iran’s defense-security strategy [4].

The new strategy’s main force comes from the secondary sanctions, as there are few bilateral economic transactions between the U.S. and Iran. Among hundreds of measures introduced so far, two sets have been particularly damaging to Iran’s economy: those that have reduced crude oil exports to a fraction of their previous level, and those that have made financial dealings with the world increasingly difficult and costly and substantially reduced Iran’s access to a substantial portion of its official foreign exchange reserves. The secondary sanctions have in effect converted U.S. bilateral sanctions into “quasi-multilateral” ones, as very few firms or governments want to risk access to goods, services and financial markets in the U.S., the world’s largest market. That the dollar is by far the world’s most important currency, and most commodities, including crude oil and natural gas, are priced in it make the secondary sanctions particularly effective [5].

The U.S. sanctions, together with depleted macroeconomic buffers (eg, budget and balance of payments surpluses, large and accessible non-dollar foreign exchange reserves) and weak or inappropriate policy response, have had a large impact on Iran’s economy. To date, however, they have not much affected its security strategy and political objectives. Iran has refused to enter direct talks with the Trump administration on a revised JCPOA with new conditionality. The EU and non-EU countries have not been successful in maintaining the economic benefits to encourage Iran to stay in the JCPOA [6]. Since 2019, Iran has responded to the increasing sanctions and resulting economic pressures by decreasing compliance with the deal’s nuclear commitments and by conducting military and security operations in the Persian Gulf area.

Box 1. Summary of U.S. sanctions on Iran

During 2011-2015, global economic sanctions contributed to the shrinking of Iran’s economy, as crude oil exports fell by more than 50 percent, and it could not access foreign exchange assets abroad. In accordance with the JCPOA, the Obama administration waived relevant sanctions and revoked relevant executive orders (EOs); UN and EU sanctions were lifted as well. U.S. sanctions on direct trade remained in place, in response to Iran’s support for Middle East allies, human rights violations and efforts to acquire missile and advanced conventional weapons technology. UN Security Council Resolution 2231, which endorsed the JCPOA, kept in place a ban on Iran’s import or export of arms (until 18 October 2020) and a non-binding restriction on development of nuclear-capable ballistic missiles (until 18 October 2023). The sanctions relief enabled Iran to increase oil exports to near pre-sanctions levels, regain access to foreign exchange funds and order new passenger aircraft.

On 8 May 2018, President Trump announced that the U.S. would no longer participate in the JCPOA and re-imposed all secondary sanctions, as of 6 November 2018. Sanctions have since been at the core of Trump administration policy to apply “maximum pressure” on Iran, with the stated purpose in particular of compelling it to negotiate a revised JCPOA that takes into account U.S. concerns beyond the nuclear program. These sanctions are considered the most sweeping in the world. The policy has caused major companies to exit the Iranian market and created a severe recession. Iran’s oil exports plummeted, particularly after May 2019, when the administration ended exceptions for the purchase of Iranian oil. The Trump administration has also sanctioned several senior Iranian officials, as well as pro-Iranian militia figures in Iraq, Lebanon, Yemen and Afghanistan.

As of July 2020, U.S. economic and financial sanctions on Iran included:

•Ban on U.S. trade with, investment in and financing for Iran: Executive Order 12959 and the Comprehensive Iran Security, Accountability and Divestment Act of 2010 (CISADA) ban exports by U.S firms to Iran, imports from Iran or investment in Iran. Several laws and orders mandate sanctions on virtually any type of transaction with or in Iran’s energy sector.

Oil export sanctions: In 2011, the Congress sought to reduce Iran’s oil exports by imposing sanctions on financial transactions with the central bank (CBI), which is tasked with receiving Iran’s oil receipts from its worldwide sales. President Obama, in his signing statement on the bill (National Defense Authorization Act, P.L. 112-81, December 2011), indicated he would implement the provision so as not to damage U.S. relations with allies, many of which were purchasing crude oil from Iran. Thus, exemptions were given (through Significant Reduction Exemption (SRE)) to India, Japan, South Korea, Taiwan, Turkey, etc. Iran’s crude oil exports fell from an average of 2.5 million barrels per day (mbd) in 2011 to about 1.1 mbd during 2014-2016; in January 2016, the Obama administration issued waivers to implement the JCPOA, which suspended implementation of the country level SREs for oil purchases. Iran’s crude oil exports rebounded to about 2.5 mbd by May 2016. As the Trump administration withdrew from the JCPOA, the SREs went back into effect in November 2018; Iran’s crude oil exports fell to about 1.6 mbd by October 2018 and to less than 0.5 mbd by May 2020, as SREs were ended under the “maximum pressure” strategy.

Ban on foreign assistance: U.S. foreign assistance to Iran — other than purely humanitarian aid — is banned under §620A of the Foreign Assistance Act. Iran is also routinely denied direct U.S. foreign aid under the annual foreign operations appropriation acts.

Restriction on exports to Iran of “dual use items”: Primarily under §6(j) of the Export Administration Act (P.L. 96-72) and §38 of the Arms Export Control Act, the U.S. denies license applications to sell Iran goods that could have military applications.

Sanctions against lending to Iran: Under §1621 of the International Financial Institutions Act (P.L. 95-118), U.S. representatives to international financial institutions, such as the World Bank and the International Monetary Fund (IMF), are required to vote against loans to Iran by those institutions.

Restrictions on Iranian shipping: Under Executive Order 13382, the U.S. Department of the Treasury named Islamic Republic of Iran Shipping Lines and several affiliated entities as entities whose U.S.-based property is to be frozen.

Banking sanctions: During 2006-2011, several Iranian banks were named as nuclear proliferation or terrorism supporting entities under Executive Orders 13382 and 13224, and CISADA prohibited banking relationships with U.S. banks for any foreign bank that conducted transactions with Iran’s Revolutionary Guard or with sanctioned Iranian entities. The defense authorization for fiscal year 2012 (P.L. 112-81) prevented U.S. accounts with foreign banks that processed transactions with Iran’s CBI (with specified exemptions). This list was expanded to include the entire financial sector of Iran on 8 October 2020. The Trump administration announcement indicated that 18 additional Iranian banks were to be sanctioned, following a 45-day wind down period.

Source: Kenneth Katzman, “Iran Sanctions,” Congressional Research Service (Updated 23 July 2020; Ian Talley, “The US Sanctions Additional Iranian Banks.” Wall Street Journal, 8 October 2020. For an up-to-date list of U.S.-imposed sanctions on Iran, see www.state.gov/iran-sanctions/.

The COVID-19 pandemic has prompted international criticism of the U.S. sanctions, which have weakened Iran’s health system. Tehran has reported more cases and deaths than any other country in the Middle East [7]. Numerous accounts indicate that sanctions have prevented it from financing medical equipment, even though the sanctions are not supposed to apply to humanitarian transactions. Iran has applied to the IMF for a $5 billion loan, but the Trump administration has threatened to vote against it (though it does not have veto power) if the IMF’s Board of Executive Directors considers the request.

III. SOME HISTORICAL BACKGROUND

Since the 1979 revolution that toppled the monarchy and the creation of the Islamic Republic, Iran’s economic and political dynamics have created domestic gridlock, international hostility and isolation. President Hassan Rouhani, who took office in mid-2013, attempted to break this cycle through the JCPOA. It was hoped that Iran would then be able to harness its vast natural resources and human capital over five to ten years to address the main con- straints and produce an extended period of rapid economic growth.

Sanctions have been a significant component of U.S. policy toward Iran since 1979. In the 1980s and 1990s, they sought to compel Iran to cease what the U.S. and its Middle East allies viewed as acts of hostility and to limit its strategic power in the region. After the mid-2000s, U.S. and international sanctions focused on trying to persuade Iran to agree to limits on its nuclear program.

In the years before the Islamic Revolution, the economy was transformed from a largely rural system into that of a complex industrial country with much higher per capita income. Education, health, social protection and infrastructure vastly improved. Iran also developed a host of institutions to support economic development and allow capital, labor and product markets to grow in size, scope and depth. Much of this transformation resulted from ability to engage in global markets. Iran sent thousands of students to European and U.S. universities and imported technology, capital and intermediate goods. Oil revenues played a major role in facilitating those imports, but also meant that Iran failed to harness what it learned by more intensively developing production for non-oil exports. The oil and gas sector dominated the industrial sector, and its contribution to GDP and the resulting foreign exchange permitted, at least at times, a higher standard of living (see Figure 1).

Manufacturing never dominated the economy in the decades before the revolution, largely because of an overvalued exchange rate brought about by “Dutch disease” [8]. Nevertheless, Iran enjoyed high economic growth and relatively low inflation until 1976-77, when the economy overheated as a result of massive development and military outlays and emerging bottlenecks, as well as increased income inequality.

Global forces that enabled substantial oil revenues led to growth of the private sector, particularly in consumer products and food processing, and of the service sector, which helped develop human capital, infrastructure and institutions. The basic infrastructure and some heavy industries that were built in this period facilitated economic diversification in the 1990s and early 2000s.

This growth came to an abrupt end starting in 1977 – during the following four years ran’s real GDP fell by about 60 percent (cumulatively) due to social and political upheaval, revolution and start of the Iran-Iraq war. Four decades later, the economy has undergone important structural changes. Though oil dependency continues, particularly in terms of fiscal revenues and foreign exchange earnings, the economy is more diversified. The share of oil and gas in GDP declined from around 25 percent to 12.5 percent by 2019, by which time the manufacturing and mining sector’s value-added exceeded that of the oil and gas sector.

These changes are in part a result of the economic and political isolation caused by years of U.S. trade and financial sanctions. The increased diversification in production and exports (though non-oil exports have been dominated by petrochemical products) has been supported by significant improvements in human development and other social indicators and increased technological capabilities, despite massive brain drain [9]. The investment climate has been weak, however, beset by uncertainty; public finances and banking remain fragile; and the economy, dominated by the public sector, continues to be inward looking and unsure of its global position, even as trade and financial relationships with neighbors (particularly Iraq and Turkey) and East Asia (particularly China), grew stronger over the last decade.

Macroeconomic performance since the revolution has reflected some of the internal tensions and external dislocations experienced by the economy, as Iran has gone through cycles of populism and pragmatism, driven by vicissitudes in the international oil market. Iranians have seen their living standard decline over the last decade, both in GDP per capita and relative to the average GDP per capita income for upper-middle income countries. However, this relative deterioration appears to have started in 2006-2007 (when oil prices exceeded $80 per barrel) and worsened from 2012 onward, with imposition of international sanctions (see Figure 2).

Persistent cycles of slow growth and high inflation cannot be resolved without fundamental institutional changes and reform of the governance system. Whether and when these challenges will be met will depend only partially on the design and adoption of appropriate economic policies, important as they are. The experience under both the first (1988-1993) and third (2000-2005) five-year plans — during which there were some bouts of growth — points strongly to the economy’s responsiveness to economic reforms and the need for a far-reaching, comprehensive package of political and institutional reforms. Delaying these can only add to the costs and pains of future adjustments [10].

IV. IRAN’S VULNERABLE ECONOMY BEFORE THE JCPOA

As a result of many years of sanctions in the 1980s and 1990s, economic growth was significantly below its potential and suffered from relatively high inflation. Real non-oil GDP grew at 2-3 percent a year, and inflation averaged more than 12 percent in 1995-2005. After some reforms during President Khatami’s administration, growth accelerated to around 5.5 percent a year. During much of the subsequent period (2005–2010), however, policies were inadequate or inappropriate to produce macroeconomic stability. In addition, despite relatively high oil prices that led to a sharp increase in oil revenues, a deteriorating business climate, governance issues and worsening regional security issues prevented a rebound in private sector investments; GDP growth remained subdued (around 4 percent a year), and inflation and youth unemployment rates remained high.

Due to the nuclear-related international sanctions in 2012-2015, real oil GDP contracted by 36.5 percent in 2012 and 5.1 percent in 2013. Non-oil real GDP, growing by 5.3 percent a year during the previous decade, grew by less than 0.5 percent a year in 2012-2015 (see Table 1). Real GDP fell for a second consecutive year in 2013, shrinking by about 0.5 percent after having contracted by almost 8 percent in 2012. The economy emerged from recession in 2014, as real GDP grew about 3.2 percent, but under the weight of international sanctions, suffered a further decline of 1.6 percent in 2015.

By mid-2015, when the JCPOA was reached, and oil export sanctions were lifted, oil prices, which had suffered a sharp decline in 2014, were still substantially below their pre-2014 level. Even after the agreement, IMF and World Bank medium-term projections for Iran’s economic growth were somewhat subdued, at around 4 percent a year. Faster growth would have required deep and sustained economic reforms that built on the JCPOA. It was assumed that the successful and timely implementation of the agreed measures by both sides would eventually lead to these.

Inflation, which had reached 35 percent in 2013, declined to about 12 percent in 2015. But the sharp decline in oil prices and continuation of some sanctions (particularly in the financial and banking areas) forced the government to follow an expansionary macroeconomic “stimulus package” policy [11]. Despite countercyclical policies in 2015, inflation decelerated in 2015–2017, averaging about 10 percent a year. A moderate budget deficit (largely a result of higher oil revenues), relatively tight monetary policy and reduced exchange rate volatility explain this deceleration.

Real exchange rate depreciation continued to provide impetus to sectors such as agriculture, parts of manufacturing and non-oil exports. Manufacturing sector performance improved as a whole after lifting of sanctions. Its value-added in real terms grew an average of 6 percent in 2016-2017 per year. But private sector growth in real capital formation in machinery remained subdued, and overall real private investment fell nearly 25 percent in 2015-2016, recovering only marginally (1.6 percent) in 2017.

The medium-term outlook in 2015-2017 remained highly uncertain, subject to several downside risks. In particular, the increasingly fragile banking and financial sector was burdened by a high level of non-performing loans, rising fiscal and financial pressures from the seriously underfunded pension system and an unregulated and highly leveraged shadow banking sector outside the elected government’s purview [12]. The continuing failure to address high youth unemployment presented additional downside risks in the form of potential social tensions.

The IMF argued to the Iranian authorities in their policy dialogue prior to U.S. withdrawal from the JCPOA that comprehensive structural reforms were needed to improve the business environment; enforce budget constraints; restructure the corporate sector to reduce dependence on subsidies and energy-intensive production; promote private sector investment; allow the financial sector to better allocate savings and handle risks; and address high unemployment [13].

Experts at international financial institutions and private consulting firms familiar with the economy in 2016-2017 argued that because it was well diversified, with a young, educated labor force and a large domestic market, Iran had a good starting point to advance such reforms [14]. However, its institutional policy and regulatory frameworks for product and labor markets lagged, reducing global competitiveness. Indeed, deep reforms have been urgently needed over the last decade to improve the business environment so as to attract foreign direct investment (FDI) and domestic private investment, boost productivity and help restore growth and employment generation. Given the economy’s vulnerable state — barely recovering from the 2012-2015 international sanctions — the return of U.S. sanctions was a serious set-back, but it also made the need for long-term vision and political will to undertake fundamental reforms and rebuild the country’s macroeconomic buffers even more urgent.

An important lesson that has emerged from international experience with economic and financial sanctions, including Iran’s, is that their impact can vary by the targeted country’s prior conditions and the nature of the policies it pursues both before and during sanctions. Weak initial conditions and an inappropriate macroeconomic policy response are likely to magnify the adverse impact. The external economic environment is an additional factor to consider. For example, weak global and regional economic conditions that result in lower trade and declining oil prices can amplify the adverse impact.

V. MACROECONOMIC IMPACT OF TRADE AND FINANCIAL SANCTIONS, 2012-2019

Assessing the economic situation in Iran is challenging for several reasons. The quality and timeliness of official statistics are weak; statistics may exclude industrial activities related to defense and security; and activity in the large informal economy is not measured [15]. In addition, Iran has a big underground economy (distinct from the informal economy), which includes illicit trade and smuggling — activities that presumably grow under sanctions. Another complicating issue is that Iran uses its own calendar (the Iranian year usually begins within a day of 21 March of the Gregorian calendar at the vernal equinox), which could result in misinterpretation of economic indicators and their timing.

Official statistics from different sources provide widely divergent figures. The central government’s budget is published, but data on fiscal operations have not been publicly available since 2017, and the data that are publicly available pertain to the central government rather than the public sector as a whole. The full extent of the public sector’s debt and contingent liabilities, therefore, is not clear [16].

Sanctions and Open-Economy Macroeconomics

One way to combine the qualitative analysis by political scientists and the quantitative analysis of economic impact and effectiveness is to treat sanctions as macroeconomic policy choices analogous to monetary and fiscal policies. One scholar has proposed an open economy macroeconomic model to assess impact [17]. Transmission of policy effects by the sanctioning country on the target country through trade and financial channels could be used as a form of economic threat or coercion that certain policy or behavior, if not reversed, could result in substantial welfare losses in the target country, while minimizing any significant adverse economic impact on the sanctioning or sender country (or countries).

Within the framework of open-economy macroeconomics, the transmitted effect is thus a policy shock. The macroeconomic impact typically operates through two interrelated transmission channels: trade and finance. Impacts show up after imposition of sanctions on the target country’s terms of trade and balance of payments. The impact on its exchange and inflation rates is more or less immediate, unless the targeted country has a relatively large and self-sufficient economy; maintains significant, internationally diversified trade and financial links with the rest of the world; or has significant macroeconomic buffers (such as a fiscal surplus, a large current account surplus with substantial official foreign exchange reserves and/or a well-endowed sovereign wealth fund).

Estimating the Effect of Sanctions on Iran

The effect of sanctions on Iran can be estimated in various ways. Estimates of key macroeconomic indicators during Sanctions I (2012-2015) and Sanctions II (2018 to the present) can be compared with the economy’s “long-term” (1995–2011) prior performance, as well as with other comparators, such as model-based pre-sanctions medium-term forecasts for 2012-2019. Iran’s performance under sanctions can also be compared with that of Russia and Venezuela, two other oil-exporting countries affected by international sanctions. Likewise, macroeconomic policy responses by the authorities, both before and during the sanction periods, as well as external economic conditions, including the international price of oil and global economic growth, can be examined.

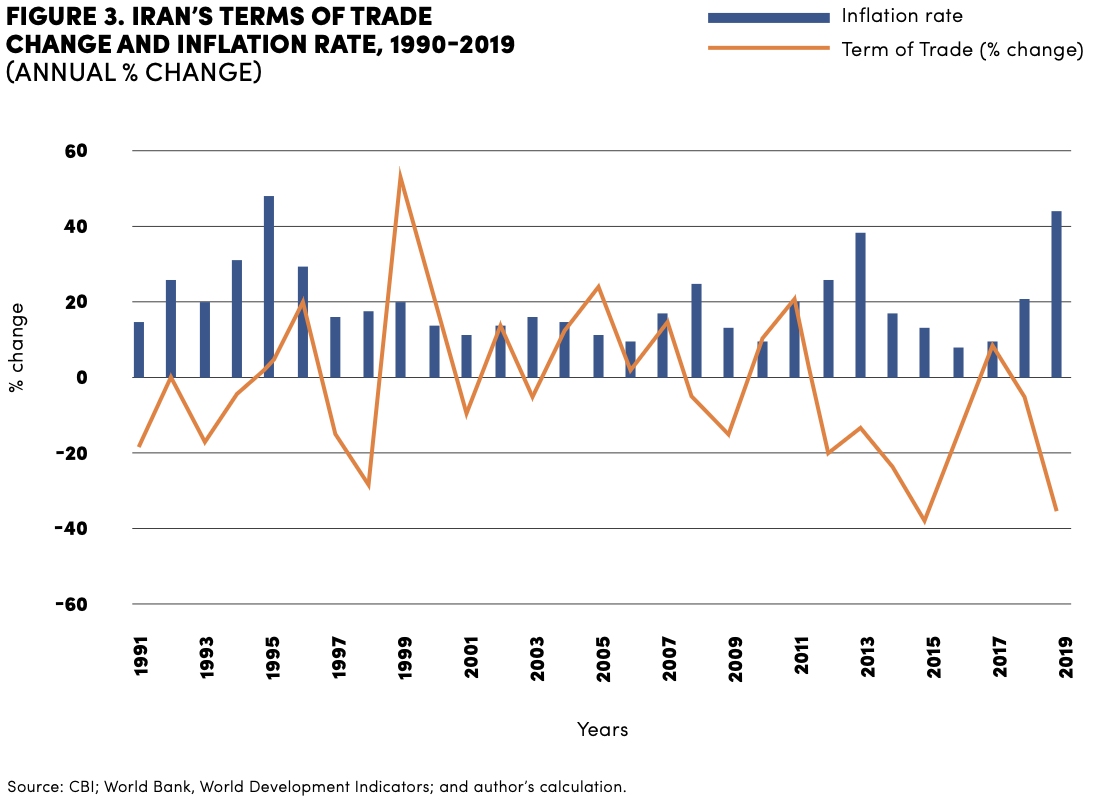

Iran is highly dependent on oil exports, and its balance of payments is very sensitive to changes in international oil prices. Terms of trade deteriorated sharply in the last few years, in part because of oil prices’ sharp decline, in part due to sanctions’ impact on its exchange rate and import prices. Terms of trade deteriorated by more than 50 percent between 2017 and 2019, and rising import prices reinforced inflationary pressures.

Iran’s financial links to the world and its ability to import intermediate and capital goods are crucial to the functioning of its non-oil export industries, as well as the operational maintenance of its oil and gas sectors. Its macroeconomic buffers eroded markedly during the long periods of sanctions, as export revenues fell sharply, leading to further import cutbacks since 2017 (see Figure 4).

While during the pre-JCPOA 2012-2015 sanctions Iran was able to export about 1.2 mbd, and oil prices remained high (particularly 2012-2014), its crude oil exports have been reduced under current sanctions to about 0.5 mbd. At the same time, oil prices are much lower than in 2012-2014 due to a substantial excess supply of oil worldwide.

Macroeconomic performance during Sanctions I and Sanctions II

Sanctions II (the U.S. “maximum pressure” strategy) has had a much more severe effect on the economy than Sanctions I (international sanctions by the EU, U.S. and UN) [18].

The impact of Sanctions II on oil GDP and oil exports has been substantially larger than the impact of Sanctions I:

real oil GDP fell by about 9 percent per year during Sanctions I but by 28 per cent per year during Sanctions II;

oil export proceeds during Sanctions II were lower than Sanctions I by about 30 percent ($40 bil. a year compared to $55 bil. a year), but this was mainly due to lower oil prices; however, it is projected that oil revenues could fall below $20 bil. in 2020, since crude oil exports have dropped to around 0.5 mbd (compared to 1.2 mbd during Sanctions I).

During 2018-2019, the decline in real GDP was more than 3.5 times that under pre-JCPOA sanctions (2012-2012), as real GDP growth averaged -5.9 percent (2018-2019) compared to -1.6 per cent in 2012-2015; however, not all these declines were the direct result of sanctions. Lower oil prices and the government’s macroeconomic policy response may have contributed to deepening of the recession.

The impact on inflation was 58 percent larger under Sanctions II (36.1 percent compared to 22.8 percent).

The impact on the real effective exchange rate was more than eight times larger during Sanctions II.

While the official exchange rate remained pegged to the US dollar at 42000 rials per dollar, in the parallel market the rial lost nearly 85 percent of its value against the dollar between mid-2019 and mid-2020.

The declines in private consumption and the ratio of gross domestic fixed investment to GDP were substantially greater.

The central government’s fiscal deficit was nearly four times larger; public debt to GDP more than doubled under Sanctions II, a clear sign of fiscal dominance.

A combination of poor policy response (mainly failure to adopt early meaningful fiscal and banking reforms and poor exchange rate policy which failed to act as a shock absorber for the economy) and the loss of public confidence in the government’s ability to deal with the economic and social ramifications of the sanctions resulted in a more than 200 percent increase in the premium on the market exchange rate of the rial against the dollar relative to the official exchange rate. The premium – just 20 percent during Sanctions I — has more than doubled in the first nine months of 2020 [19].

Official reserves are estimated at about $100 billion, but the extent to which the government has immediate access to them is not clear. According to a former U.S. special representative for Iran, it may have access to just 10 percent [20]. The most recent IMF estimate for immediately accessible foreign exchange reserves in 2020 is around $10 billion, or only about two months of imports.

Though Iran has been able to maintain or even increase its non-oil exports during recent years, balance of payments pressures have built up due to the severe impact of sanctions on oil export proceeds, which are projected to decline to about $20 billion in 2020, from an average of about $40 billion a year in 2018-2019. Moreover, global recession and the Covid-19 pandemic’s impact on trade have had a significant negative effect on Iran’s efforts to increase its non-oil exports in 2020.

Capital outflow continued unabated during the two sanction periods, amounting perhaps to as much as $100 billion during 2012-2019; however, some of this may be export proceeds stranded overseas due to the re-imposition of the financial/banking sanctions on Iran [21].

As indicated earlier, Tables 1 and 2 show Iran’s key macroeconomic indicators during the two sanctions episodes. Table 2 summarizes the different approaches utilized in this paper to calculate the potential macroeconomic impacts of sanctions on Iran during 2012-2019. Obviously, as argued earlier, not all of Iran’s economic performance during this period can be attributed to sanctions, as the economy’s initial conditions, the nature and quality of the authorities’ macroeconomic policy response and the external environment also contributed to overall performance.

Nevertheless, sanctions on oil exports, banking and finance clearly played a more important role than other factors in adversely affecting the performance of Iran’s economy, particularly during much of the period 2012-2019. This contention is supported by a large body of academic literature.

The increasing interdependence and complexity of the global trade and financial systems mean that many factors other than comparative advantage in trade impact sanctions’ effectiveness. One is the number of countries imposing them. The more countries, or multinational organizations, the more effective a sanctions regime is likely to be. On average, multilateral sanctions tend to decrease the targeted country’s real annual GDP per capita growth rate by more than two percentage points, while unilateral sanctions tend to decrease the targeted country’s real GDP per capita by around 1 percentage point per year. A detailed review of relevant cross-country academic literature is presented in Appendix A. A review of selective quantitative studies on Iran’s experience with economic sanctions is presented in Box 3.

Box 2. Summary of Iran’s Economic Performance During Sanctions I and II and in Comparison to Historical Trends

Pre-Sanctions I and II: historical performance (1995-2011)

Output growth: 4.1 percent a year

Oil income: $60 billion a year

FDI inflows: $1.4 billion a year

Inflation: 18.5 percent a year

Private consumption growth: 4.9 percent a year

Private Investment growth: 8.8 percent a year

Sanctions I (2012-2015) – over four years (cumulative)

Output loss: 25 percent

Oil income loss: $237 billion

FDI loss: $20 billion

Inflation: 13.5 percentage points in additional inflation per year, compared with average inflation in 1995-2011

Private consumption fell by about 8 percent

Private investment fell by about 28 percent

Sanctions II (2018-2019) – over two years (cumulative) but continuing in 2020

Output loss: 20 percent

Oil income loss: $80 billion

FDI loss: $12 billion

Inflation: 24 percentage points in additional inflation per year, compared with average inflation in 2016-2017

Private consumption fell by 9.8 percent

Private investment fell by 6.8 percent

Source: Tables 1 and 2 and Appendix B.

Long-term effects of sanctions

Because myriad factors determine growth in an economy, isolating the effect of sanctions on long-term growth is difficult. Depressing an economy for years and preventing it from reaching its full potential output will depress growth even after sanctions end, because time is needed to rebound and rebuild. Fighting sanctions also forces a country to expend considerable resources, such as foreign exchange reserves, leaving it more vulnerable to future external shocks and less able to stabilize.

Sanctions also affect long-term growth by delaying needed reforms. During a crisis, there is little political will to implement policies promoting long-term growth. As a result, structural reforms are shelved. Additionally, if the costs of sanctions are high enough, the economic and societal paradigm may shift so much that even after sanctions are lifted and political will on the part of the authorities is more inclined toward reforms, there may be no realistic way to implement long-term growth policies, because the economic environment is not sufficiently stable or strong enough to support them.

This issue is particularly relevant to Iran. Even though the sanctions have forced Iran to become more self-reliant, the longer-term adverse impact of sanctions on the economy are likely to be substantial. The decline in real per capita income — estimated to be as much as 30 percent during 2012-2019 — has already led to a substantial erosion of living standards for the middle class and the vulnerable and poor segments of the population. The substantial drop in investment — private, public and FDI — during the past decade implies a significantly lower output growth in coming years, because of expected declines in both labor and total factor productivity growth rates.

Fiscal and monetary policies and the issue of fiscal dominance

The main mission of monetary policy is to conduct countercyclical policy while controlling inflation. In practice, central banks often pursue other goals. Developing countries, particularly oil-exporters, often engage in procyclical fiscal and monetary policies during boom periods, which tend to amplify the impact of positive commodity price shocks. The practice often increases inflationary pressures and forces the exchange rate to appreciate in real terms. In Iran, fiscal policy and the manner of financing government expenditures have had a very significant effect on monetary policy and its impact on inflation. Recent empirical evidence indicates that fiscal and monetary policies have generally been highly expansionary, particularly during economic booms, often resulting in subsequent large exchange rate depreciations followed by higher inflation rates and economic slowdown.

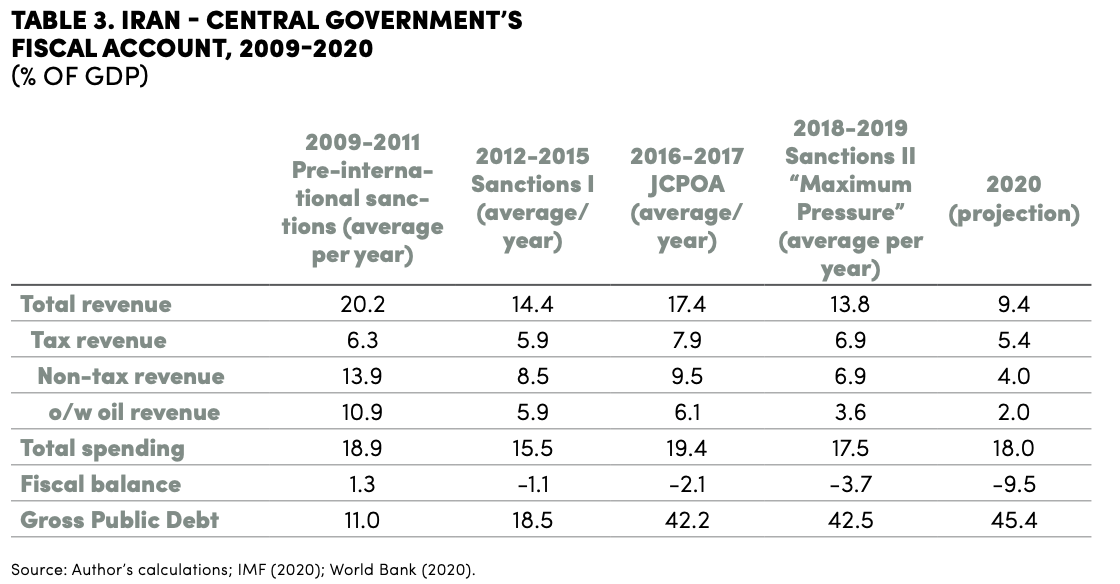

A structurally balanced fiscal rule that maintains an aligned exchange rate allows effective countercyclical monetary policies and discourages excessive foreign financing. Policy measures that increase reliance on domestic resources make the economy more resistant to external shocks. In Iran, fiscal pressures, which have been building during 2018-2019, will inevitably dominate monetary policy [22]. This is particularly relevant as sanctions are projected to further reduce oil export proceeds by almost 50 percent in 2020. Under conditions of fiscal dominance, monetary policy becomes less effective, as both its targets and instruments no longer fall under the full control of the central bank (see Table 3).

Given the contractionary economic impact of the COVID-19 pandemic and the limited scope for raising non-oil revenues because of the global recession, the government’s expenditure polices are likely to remain the key economic policy tool in Iran in the next few years, as both tax revenues and oil revenues have fallen sharply since 2016. Accordingly, the budget deficit and the level of public debt are likely to increase in 2020.

Though the government aspires to cover its increasing financing needs through an enhanced program of selling treasury instruments and offloading assets on the stock exchange, recourse to monetary financing and National Development Fund resources is likely to rise. The increase will be inflationary, because this approach to financing the budget deficit will increase the monetary base [23]. Moreover, as long as the high degree of fiscal dominance continues, significant increases in interest rates to choke off inflation could raise the risks of public debt becoming unsustainable, in part due to massive contingent liabilities of commercial banks and the pension system.

Alternative estimates of some of the economic costs of sanctions

As indicated in the previous section, official data suggest that under Sanctions I Iran’s per capita real income fell by about 12 percent – about 2.8 percent a year — between 2012 and 2015 (Table 2). More worrisome is that by 2019, the level of real GDP was almost 50 percent lower than its projected historical trend. The use of alternative measures such as synthetic control to construct a counterfactual for Iran, suggests that the actual level of real GDP in 2019 was about 46 percent below what it would have been that year had the economy grown at the rate of “synthetic Iran” [24].

As a result of the economy’s contraction, the per capita real income of Iran’s citizens in 2019 was nearly 30 percent lower than it would have been had sanctions not been imposed in 2012-2019. Moreover, real private consumption, which grew by about 5 percent a year during 1995–2011, declined by 1.5 percent a year during 2012-2019, a cumulative decline of about 12 percent. The ratio of gross fixed investment to GDP fell by 11.3 percentage points, 2011-2019. The last times private consumption and investment fell by such magnitudes were during the 1979 revolution and the 1980-1988 Iran-Iraq war.

Continuation of the U.S. “maximum pressure” strategy, combined with devastating COVID pandemic-related losses, is likely to result in another 6 to 8 percent reduction in Iran’s per capita real income in 2020, increasing poverty and inequality and possibly creating a humanitarian crisis. Box 4 summarizes the macroeconomic measures introduced in response to the pandemic disaster, which clearly are hardly adequate. Nevertheless, the government’s weak fiscal and balance of payments position does not allow it to be more aggressive in countering the pandemic’s adverse effects (for a list of potentially more appropriate policy responses see Annex C).

Comparison of Effect of Sanctions on Iran, Russia and Venezuela

Effect of International Sanctions on Russian Federation

Comparison of the effects of sanctions on Iran and Russia provides useful lessons. Iran was targeted by both the U.S. and the UN with severe sanctions in 2012, in an effort to force it to suspend uranium enrichment-related and reprocessing activities and cooperate with the International Atomic Energy Agency (IAEA). These froze the assets of key individuals and companies related to the nuclear program, banned supply of nuclear-related materials and technology to Iran and targeted access to the international oil and financial markets. In response to its actions in the Crimea and Ukraine, Russia was targeted much more narrowly in 2014 by a smaller group of countries: mainly the U.S.; the EU imposed a limited number of sanctions.

The main difference in the experiences of Iran and Russia with sanctions is that the most important pillars of Iran’s economy were hit, whereas Russia was more or less able to continue doing business as before. Iran, which depends on oil exports, was no longer able to access the global oil market; nor could it access its assets held abroad to support the economy or find outside financing for stabilization. In contrast, sanctions in Russia banned a few individuals and entities close to the Putin administration from accessing international financial systems (through asset freezes and the banning of investment in some companies). Most aspects of the economy, however, were relatively unaffected.

The difference in the nature of the sanction regimes led to vastly different experiences. Iran’s economy was heavily damaged; Russia fared far better. Iran experienced significant economic contraction under both rounds of sanctions; Russia experienced a slowdown in economic growth but not a contraction.

Inflation and unemployment tell a similar story. Iran saw significant deterioration of both indicators. The impacts on its human development and poverty have also been much more severe than in Russia. The sharp acceleration in inflation had a major adverse impact on the poor and vulnerable, as well as the middle class. Lack of adequate access to medical supplies and pharmaceuticals, together with a sharp deterioration in economic conditions, has led to social and political instability. But Russia, while experiencing an increase in poverty, has been able to use its policy arsenal and macroeconomic buffers to moderate the damage to its economy and healthcare system. Likewise, differing levels of economic and welfare impacts led to different political outcomes. Russia did not alter its foreign policy, while Iran is perceived to have been pressured into agreeing in the JCPOA to halt major parts of its nuclear program in exchange for sanctions relief.

Effect of U.S. Sanctions on Venezuela

The U.S. has imposed sanctions on the Venezuelan government and individuals for more than a decade. The Trump administration significantly expanded these and also targeted the state oil company and central bank. In 2020, the U.S. Treasury sanctioned two subsidiaries of the Russian state-controlled Rosneft Oil Company for facilitating Venezuelan oil exports and four shipping companies for transporting Venezuelan oil. As of 20 August, it had imposed sanctions on more than 150 Venezuelan or Venezuelan-connected individuals, and the State Department had revoked the visas of more than 1,000 individuals and their families. The administration has also promised to continue to support National Assembly President Juan Guaidó, whom nearly 60 countries recognize as interim president. While all this has increased economic pressure, accelerating a decline in oil production, Nicolás Maduro remains in power nearly three years after the U.S. stopped recognizing his presidency.

Most of the impact of the US imposed on Venezuela has been on civilians, reducing caloric intake, increasing disease and mortality for both adults and infants and displacing millions, who fled the country due to worsening economic depression and hyperinflation. Sanctions exacerbated the economic crisis, making it nearly impossible to stabilize the economy. The economy’s collapse and hyperinflation disproportionately harmed the poorest and most vulnerable and resulted in more than 40,000 deaths in 2017-2018. Even more destructive than the broad August 2017 sanctions were those imposed by executive orders in January 2019 and in 2020:

[T]hese sanctions would fit the definition of collective punishment of the civilian population as described in both the Geneva and Hague international conventions, to which the United States is a signatory. They are also illegal under international law and treaties which the United States has signed, and would appear to violate U.S. law as well [37].

Although the sanctions against Iran, Russia and Venezuela had differing scope and degree of severity, three lessons may be drawn from their experiences over the last few years. Timely and appropriate macroeconomic response can reduce the size and duration of the adverse shock (Russia); greater diversification of the economy and exports and a functioning private sector could make the targeted economy more resilient (Iran and Russia); and having relatively large and accessible external buffers (e.g. official foreign exchange reserves) could limit the damage on the local economy (Russia).

Box 3. Results of selected quantitative studies related to sanctions on Iran

Several rigorous investigations estimate the macroeconomic and or trade costs of the international sanctions on Iran’s economy. While nearly all the following quantitative studies were prepared prior to the “maximum pressure” U.S. sanctions, they remain relevant, as they shed light on different aspects of macroeconomic impacts of sanctions using different methodologies. It is quite clear that the trade and financial sanctions imposed on Iran over the last three decades have caused massive damage to Iran’s economy and the overall welfare of Iran’s population.

Dizaji and van Bergeijk (2013) confirm the conclusion reached by Hufbauer et al. (2009) that despite the considerable impact of the oil boycott on Iran’s economy (prior to the “maximum pressure sanctions”), the relative size of the impact tends to diminish over time [26].

Ghodosi and Karamelikli (2020) found that the adverse impact of the narrowly focused or targeted EU sanctions was milder than that of more generalized trade sanctions. Using a non-linear autoregressive distributed lag (NARDL) model, they investigated the impact of the EU measures on quarterly bilateral trade values between the 19 members of the Euro Area (EA) and Iran (1999- 2018). Their results indicated that general sanctions have strongly hampered trade flows. The impact of these on the total imports of the EA19 from Iran was more than four times stronger than on the total exports of the EA19 to Iran. Moreover, the impact of “smart sanctions” targeting Iranian entities and natural persons was much smaller than that of general sanctions on total trade values and the trade values of many sectors [27].

Farzanegan and Hayo (2019) used provincial-level data for Iran for 2001–2013 to study the impact of sanctions on the informal economy. They found that the international sanctions hurt the informal economy much more than the formal economy. The sanctions imposed in 2012/2013 not only reduced the real GDP growth rate, but also that of the “shadow economy” — by as much as 30 percentage points more than the decline in the formal economy. They concluded that sanctions can be considered a double burden on the Iranian population, since they also negatively affect the potential safety net offered by the informal economy activities [28].

Farzanegan et al. (2015) used a social accounting matrix and a computable general equilibrium model (CGE) to simulate the impact on Iran’s oil exports. Under a scenario assuming nearly 60 percent of oil exports are banned by sanctions, real GDP declines by 2.2 percentage points, imports by 20 percentage points and private consumption by 3.9 percentage points. Their results also show that sanctions impact the income distribution [29].

Felbermayr et al.(2020) use a comprehensive database on sanctions to evaluate the effects of sanctions on Iran by using the gravity model. Their empirical analysis revealed a very strong negative impact on Iran’s trade with sanctioning countries: a 55 percent reduction from the 2012-2015 sanctions. Based on these results, they quantified the general equilibrium welfare effects and concluded that if sanctions were removed, Iran’s real per capita income could rise by about 4.2 percent. The effect would have been larger had Iran not already substantially diverted trade toward China [30].

Ghasseminejad and Jahan-Parvar (2020) focused on the impact of financial sanctions on Iran’s equity markets, 2011-2016. They found that direct and industry-wide sanctions resulted in significant short- and long-term abnormal negative returns for the targeted firm or industry, and that the negative effects were stronger for politically-connected entities. They also found evidence that the first sanctions against targeted (politically-connected) firms tended to result in the “most significant pressure” [31].

Gharehghozli (2017), using the synthetic control method, found that international energy sector sanctions, 2011-2014, reduced Iran’s real GDP by more than 17 percent, with the largest drop (12 percent) in 2012 (when Iran’s oil GDP fell 36.5 per cent), confirming that much of the measured drop in economic activity was due to sanctions on Iran’s oil exports [32].

Gharibnavaz and Waschik (2018) used a CGE model with data on production, consumption and trade from the Global Trade Analysis Project (GTAP) and an augmented dataset on urban and rural households, disaggregated by income level. Their simulation of the international sanctions suggested that Iran’s government (through its budget) bore the largest share of the sanctions’ effects (transmitted through lost rents from oil production and exports), with its spending falling more than 40 percent. They also found that lowest-income rural and urban households did poorly, experiencing welfare losses of 9.3 and 5.3 percent respectively [33].

Ianchvichina, Devarajan and Lakatos (2016) used a global general equilibrium simulation model to quantify the effects of lifting economic sanctions after the JCPOA. They focused on the lifting of the EU oil embargo; reduction in Iran’s trade costs; and liberalization of cross-border imports of financial and transport services. Their results indicated that if sanctions to be lifted, Iran’s per capita welfare could rise by 6.5 percent, provided that other oil exporters cut their output to support the price of oil. The rise in Iran’s per capita welfare would be 3.9 percent if other oil exporters did not cut back on their oil production. The study also concluded that the U.S. and Europe would gain from Iran’s recovery [34].

Pelzman (2020) examined the economic effects of the sanctions the Trump administration re-imposed in 2018, with a focus on the spillover effects on the Middle East/North Africa region, China, Russia and Turkey. His analysis of recent trade patterns indicated that it is highly likely that Iran will increasingly try to circumvent the U.S. sanctions by selling its oil to China via a transfer pricing mechanism to avoid normal trade accounting, while sales to Turkey, Korea, the UAE and India may be via gold and countertrade. This research also found that changes in Iran’s trade patterns toward Asia (and away from the U.S. and Europe) may have started as early as 2005-2006 [35].

Torbat (2005) found that the trade and financial impact of U.S. sanctions in the late 1990s and early 2000s (prior to the UN sanctions that started in 20212) cost Iran about 1.1 percent of its GDP per year in 2000-2001. He concluded that those sanctions hurt Iran’s capital goods imports and non-oil exports, and that further damage to Iran’s economic growth was caused those measures that had prevented Iran from borrowing internationally to finance high priority oil and non-oil development projects. The author concluded that the financial damage was greater than the damage caused by the trade sanctions. He also cited earlier studies that had estimated the negative impact on Iran’s economy in the late 1990s to be between 1 percent and 3.6 percent of its GDP per year [36].

Box 4. Iran’s policy responses to the COVID-19 pandemic

Iran reported its first confirmed COVID-19 cases on 19 February 2020, in Qom. The government introduced a range of measures to limit spread of the virus: stopping flights from China; closing schools, malls, markets and key religious sites; and banning cultural and religious gatherings. On 25 March, President Rouhani announced a partial lockdown, closing businesses and government offices for two weeks and banning travel between cities. As a result, the Purchasing Managers’ Index plummeted in March and April.

Concerned about the economic damage and starting in April, the government ordered a step-by-step reopening of businesses it considered at low or average risk of spreading the virus. On 27 April, all international borders were reopened to revive regional trade, and in mid-May mosques and schools were reopened. On 26 May, all businesses and major religious sites were reopened. The Purchasing Managers’ Index suggested that industries had started to recover in May and June, but it registered a 6 percent contraction in July.

A second wave of virus cases hit during the summer. In response, the government instituted mandatory mask-wearing and new restrictions in Tehran. These closed all schools and universities, restaurants, cafes, cultural facilities and beauty salons, while a third of all government employees in the capital worked remotely.

With new infections above 3,000 a day, Iran appeared to be in the grip of a third Covid wave in September. Border crossings with Iraq were sealed to prevent Iranian pilgrims from traveling for the annual 7 October Arbaeen pilgrimage. Tehran and six other provinces closed recreational centers, universities, schools and other places at high risk of contagion for a week to stem the spread. Face masks became compulsory in public (indoors and outdoors) in Tehran starting 10 October, with fines for breaches.

As of 8 October, Iran had taken the following policy measures:

Fiscal policy. Key measures include (a) extra funding for the health sector (2 percent of GDP); (b) cash transfers to vulnerable households (0.3 percent of GDP); (c) support to the unemployment insurance fund (0.3 percent of GDP); and (d) subsidized loans for affected businesses and vulnerable households (4.4 percent of GDP). The government also announced a moratorium on tax payments for three months (6 percent of GDP). Sukuk bonds, the National Development Fund and privatization proceeds will provide part of the financing. To generate income as it struggles with the economic consequences of COVID-19 and U.S. sanctions, the government on 15 April embarked on its biggest-ever initial public offering, selling its residual shares in 18 companies (including a 12 percent share of the Social Welfare Fund, SHASTA, Iran’s largest public company). The proceeds are estimated at about 165 trillion rials (0.6 percent of GDP) from banks and insurance companies and 70 trillion rials (0.2 percent of GDP) from SHASTA. On 3 May, the government’s spokesperson said shares of four state-owned oil refineries would be offered to the public soon. By the end of August,13 percent of business applicants affected by the pandemic had received part of the aid package, and 56.5 trillion rials ($245 million) had been paid from the National Development Fund of Iran.

Monetary and macro-financial policies. The CBI announced an allocation of funds to import medicine; agreed with commercial banks that they post-pone for three months repayment of loans due in February 2020; offered temporary penalty waivers for customers with non-performing loans; and expanded contactless payments and increased limits for bank transactions in order to reduce circulation of banknotes and exchange of debit cards.

Exchange rate and balance of payments. In mid-2020, the CBI announced that it had injected $1.5 billion into the foreign exchange market to stabilize the rial. In July it injected another $1 billion. In September it announced that it would put aside 1 percent of the sovereign wealth fund to stabilize the stock market.

Source: IMF Policy Tracker, Policy Responses to COVID-19 as of 8 October 2020. https://www.imf.org/en/Topics/imf-and-covid19/Policy-Responses-to-COVID-19.

VI. CONCLUSION

The estimated impact of the U.S. “maximum pressure” campaign (Sanctions II, 2018 to the present) has been very large and costly, in both human and economic terms. It would have been significant even had Iran adopted an appropriate macroeconomic response, because the economy remains dependent on oil revenues. By reducing its oil exports from about 2.5 mbd to around 0.5 mbd, sanctions seriously weakened Iran’s fiscal and balance of payments positions, leading to higher inflation (as a result of the expansion of the monetary base to finance the growing budget deficit) and a sharp currency devaluation.

Had Iran undertaken serious fiscal and banking/financial reforms during 2006- 2011, however, it would have been able to reduce sanctions’ impact. If economic actors had more confidence in the government’s policies and ability to deal effectively with external pressures, the currency would not have collapsed by as much, and the inflation rate would not have been as high. Iran’s investment climate, undermined by serious governance issues and an unstable policy environment, also contributed to low and declining private investment, particularly in manufacturing, while the sharp decline in public investment, particularly since 2017, has shaken private sector confidence.

The “maximum pressure” sanctions have undermined the ability of both the public and private sectors to deal with the COVID-19 pandemic. The next 12 to 18 months will be particularly difficult for Iran, as on top of the sanctions and pandemic, the global recession and expected slow recovery are likely to constrain its oil and non-oil exports, and the level of official reserves is likely to continue to decline.

Policymakers hope they can reach an understanding with the U.S. if its incoming administration brings about foreign policy change, including in regard to the Middle East. Even if this scenario pans out, however, change will more likely occur gradually, rather than quickly and in a significant manner. Given the serious humanitarian crisis Iranians face, the most feasible improvements would probably involve removal of some restrictions on oil exports and international banking and allowance of financial assistance from international financial institutions for purposes related to COVID-19.

APPENDICES A-D

Appendix A. Brief Review of Sanctions Literature

Economic sanctions are a foreign policy tool aimed at altering the behavior of governments or political actors in countries that violate international norms and treaties or threaten the interests of sanctioning countries. “At the beginning of the 21st century, the same as a century earlier, economic sanctions remain an important yet controversial foreign policy tool.” Have they achieved their objectives? What are their economic costs in a world increasingly interconnected via global value chains and multinational enterprises? [38]

Critics posit that they are often ill conceived and usually fail. Supporters claim they are an effective, efficient foreign policy response to crises in which national interests are in peril, and military action is not a viable option [39]. Some proponents argue that they provide a visible, potentially less expensive alternative to military intervention or doing nothing [40]. Recently imposed economic sanctions such as those against North Korea, Russia, Venezuela and Iran illustrate the diversity of objectives, seeming to provide support to arguments by both sides [41].

The U.S. and EU perceived sanctions as a means to induce Iran to negotiate over its nuclear program, a tactic to slow the development of that program and a way to force a change in domestic policies on human rights. Based on UN Security Council Resolution 1696, the first nuclear-related economic sanctions against Iran were initiated in 2006, then extended and tightened in subsequent years. Starting with trade in goods that could be used in the nuclear and ballistic missile programs, they were extended by expanding the range of goods and by financial sanctions and travel bans on individuals.

How prevalent are sanctions?

The Global Sanctions Data Base (GSDB) is an innovative tool that covers 720 publicly traceable, multilateral, plurilateral and bilateral sanction cases from 1950 to 2016. Its data show that sanctions became more popular between 1950 and 1990, then increased in the early 1990s and became yet more widespread beginning in 2004 [42].

In most cases, economic sanctions are used to interfere in a country’s decision-making process without the immediate introduction of military force. Usually imposed by large countries that pursue an activist foreign policy, such as the U.S., they have been imposed to deter objectionable actions, show resolve and assert leadership in world affairs. They became popular in recent years, because many leaders agree that “military action would be too massive and inappropriate and diplomatic protests may be insufficient” [43].

According to the GSDB’s authors, policy change and regime destabilization were the dominant objectives from the 1950s to early 1990s. However, they detect that the pattern changed dramatically from the mid-1990s onward, with the predominant aim becoming “improving human rights, ending wars, and solving territorial conflicts” [44].

Much recent academic and policy debate revolves around whether sanctions are effective in achieving stated objectives. The GSDB indicates the following: (i) until the mid-1960s, almost half of all sanctions failed; less than 30 percent succeeded; and (ii) since then, the success rate increased until the mid-1990s but has subsequently fallen sharply.

Despite increasing use, sanctions remain controversial. Many empirical studies have shown that they often fail to change behavior, because they may unify the targeted country’s population, encourage it to find commercial alternatives, and ultimately hurt firms in the sanctioning countries. Moreover, it is hard to ensure how a targeted country will respond. Cutting off strategic goods can make it vulnerable, but given the multiple sources of supply and diversified production that characterize the modern economy, that is no longer easy to do.

How can targeted countries render sanctions unsuccessful?

The interdependence of the multilateral trade system makes it difficult to implement sanctions. It has been pointed out that the “economic costs not only to the target but also to the countries that initiate the sanctions, through the loss of business contracts and a reduction or interruption in trade, undermine the economic rationale and political willingness to engage in the sanctions” [45]. Policymakers need to try to ensure that unintended effects do not spill over to products and countries not directly targeted by the barriers, causing disruptions in global and regional supply chains [46].

The existence of domestic macroeconomic buffers and alternative trading possibilities reduces a targeted country’s vulnerability to sanction shock. Domestic buffers — including fiscal space, foreign exchange reserves and social safety nets — are like hard armor when facing sanction barriers. With adequate financial resources, a sanctioned country can implement countercyclical fiscal policy in response to trade barriers, buffering the effect of sanctions on its domestic demand. If the domestic buffer is not sufficient, however, the deficit incurred by the policy will leave its economy very vulnerable, often leading to inflationary pressures, rising debt and a volatile exchange rate.

The theory of why sanctions work is rooted in the notion of comparative advantage. Different goods require different factor proportions, and different countries have different relative factor endowments. A country will export goods that are produced with its abundant inputs and import goods that use its scarce factors intensively. Trade-restricting policies will isolate a targeted country from the world market [47]. If the importance of its economic interactions with those imposing sanctions is great enough, and it lacks sufficient macroeconomic buffers and alternative trading partners, sanctions can depress income and welfare to an unsustainably low level, forcing it to comply with demands. The macroeconomic impact of sanctions on a targeted country is usually transmitted fairly quickly through a terms of trade shock (a large decline in the ratio of export to import prices), which could be magnified by a large devaluation of its exchange rate against hard currencies (eg, the dollar), and a deteriorating balance of payments position.

Macroeconomic policy response by targeted countries

The response of targeted countries can also be significant in determining the impact of sanctions. They are often able to circumvent sanctions by trading with third parties that are either not involved in the sanctions regime or refuse to abide by it. Despite repeated U.S. efforts to prevent its oil exports, for example, Iran has continued these to China and others, albeit at significantly lower levels. More recently Iran has reportedly tried to sell refined petroleum products to Venezuela for gold. The U.S. bars its citizens from buying gold in Venezuela, but Caracas sells the bulk of its gold to Turkey, reducing the sanction’s impact [48]. On the import side, countries often replace goods and services supplied by the country imposing sanctions with those from others, again limiting the effect.

Leaders of targeted countries can use sanctions to deflect blame for economic conditions and use macroeconomic buffers and adaptable, proactive fiscal and monetary policies to limit adverse economic impacts. In 2014, for example, Russia’s ruble was becoming severely devalued, inter alia due to sanctions imposed after the annexation of Crimea. In response to the worsening currency situation, the central bank abolished the dual currency trading band and fully floated the ruble. Combined with other policies, the new exchange rate system helped stabilize the currency and limit adverse economic effects.

An obstacle independent of the regime itself is the targeted country’s preparedness for external shocks. Countries have buffers to prevent unexpected macroeconomic shocks from wreaking havoc. These include sovereign wealth funds, current account surpluses, adequate international reserves (normally equivalent to 100 percent of short-term debt plus three to six months of imports), a positive and large international investment position, a flexible exchange rate regime and relatively low external debt. The extent to which these mitigate the effects of sanctions depends mainly on their initial size and sanctions’ severity.

A country with foreign exchange reserves equal to a year’s imports, for example, is in a far stronger position than one with reserves equal to only six months. A country with a large sovereign wealth fund (or a large stabilization fund) can eliminate the need to access international financial markets for government financing, mitigating the effects of sanctions to cut off access. Finally, sanctions can also hurt the country imposing them [49].

Cross-country regression results

The increasing interdependence and complexity of the global trade and financial systems mean that many factors other than comparative advantage impact sanctions’ effectiveness. One is the number of countries imposing them. The more countries, or multinational organizations, the more effective a sanctions regime is likely to be. A study that sampled 67 episodes, 1976-2012, found that bilateral U.S. sanctions had much smaller effects than comprehensive UN ones [50]. On average, the latter decreased the targeted country’s real annual GDP per capita growth rate by more than two percentage points; U.S. sanctions decreased this by just 0.75–1.0 points. UN sanctions lasted an average of ten years, leading to a total decline in GDP per capita of 25.5 percent. U.S. sanctions, which did not include secondary sanctions, reduced growth for only seven years, resulting in a total decline in GDP per capita of 13.4 percent [51].

Though multilateral sanctions, especially those imposed by the UN, are more effective than unilateral ones, there is no guarantee of success. An analysis of 22 UN sanctions regimes found they achieved at least one of the three stated goals (coercing, constraining, signaling) only 22 percent of the time. Moreover, they were far more effective in signaling a target (27 percent) or constraining activities (28 percent) than changing behavior (10 percent). UN sanctions are typically complemented by regional sanctions (59 percent of the time) and applied beside other strategies. Isolating their effect is thus hard.

Sanctions become much less effective the longer they are in place, suggesting that targeted countries can often adjust. Indeed, they tend to be most effective in the first two years, after which their impact declines steeply [52].

Vulnerability of finance to sanctions

The increase in cross-country capital flows has been driven by technological advances that allow rapid communication and information flows, along with a desire to identify foreign investments. The internationalization of finance has helped developing countries grow, by giving them access to capital not available domestically. However, it exposes them to significant loses if that access disappears due to sanctions. Outflows of capital as investors comply with sanctions can compound the effects on imports and exports and on refinancing existing debt. Sanctions can also affect domestic capital markets and financial institutions by increasing risk and uncertainty. Fewer investors and less capital tighten capital markets, decrease valuations of assets and reduce growth.

Credit risk for companies operating in sanctioned industries can dramatically increase, leading to potential difficulties for lenders. Potential investments carry more risk if the threat of sanctions remains. Uncertainty increases the risk for almost all domestic investments, as other factors (such as unemployment and inflation) dim the economic outlook. Sanctions can also reduce diversification, as financial institutions may lose access to investments in foreign markets. This effect would further increase risk, as investments would be concentrated in the domestic market, or a severely limited international market, in which only a few countries that flouted the sanctions regime would allow investment from the sanctioned country.

ENDNOTES

Security Council Resolution 2231 (15 July 2015) requires Iran to implement constraints on its uranium enrichment and heavy water nuclear reactor programs and allow the International Atomic Energy Agency (IAEA) to monitor its compliance. The agreement sought to address concern that fissile material produced in Iran’s nuclear facilities could be used to build nuclear weapons.

www.whitehouse.gov/ presidential-actions/ ceasing-us-participation-jcpoa-taking-additional-action-counter-irans-malign-influence-deny-iran-paths-nuclear-weap-on/.

For the U.S. State Department’s “fact sheet”, see www.state.gov/advancing-the-us-maximum- pressure-campaign-on-iran/. For an up-to-date list of U.S. sanctions on Iran, see www. state.gov/iran-sanctions/ and https://fas.org/sgp/crs/mideast/RS20871.pdf. For a timeline of Iran’s nuclear diplomacy, see www.armscontrol.org/fact- sheets/Timeline-of-Nuclear-Diplomacy-With-Iran.

The Trump administration has indicated that any new nuclear deal would require Iran to stop enriching uranium and halt all support to religious and militant groups in the Middle East. Secretary of State Mike Pompeo identified 12 requirements for a new agreement, noting it would require a wholesale change in Iran’s military posture in the region (Wall Street Journal, 21 May 2018).

About half of all cross-border lending and international debt securities are denominated in dollars, and nearly 85 per cent of all foreign exchange transactions are done against the dollar, which is the world’s leading reserve currency, accounting for more than 60 per cent of all known official foreign exchange reserves. More than half of international trade in any given period is invoiced in dollars, and about 40 per cent of international payments are made in them. See Bank for International Settlements (2020); and “US Dollar Funding: An International Perspective,” CGFS Paper 65. For a brief summary of the U.S. sanctions, see Box 1 below.

The European independent trade and financial channel (INSTEX), set up in early 2019, has had a slow start. It only recently began to handle transactions for medical equipment (https://www.ft.com/ content/5a647865-85e1-4919- 9a55-e852ac06f67e). Nevertheless, INSTEX can potentially help keep the nuclear agreement alive until a diplomatic solution is found to the U.S. withdrawal. In addition to demonstrating solidarity on the JCPOA, INSTEX indicates commitment to basic humanitarian principles, particularly as Iran has been hit hard by the Covid-19 pandemic.

World Bank, “MENA Crisis Tracker,” 6 October 2020.).

Dutch disease refers to situations where the export proceeds from the economy’s dominant sector cause the national currency to appreciate in real terms, thus reducing the incentive to invest in other export sectors. Such currency overvaluation, which may help keep inflation low, exacerbates distortions in the relative price of tradable and non-tradable goods and services, leads to inefficiencies in the allocation of resources and dampens prospects for new sources of growth. See Corden, W. M., and J. P. Neary. 1982. “Booming Sector and De-industrialisation in a Small Open Economy.” Economic Journal 92 (368): 825–48. This phenomenon is also referred to as “resource curse” in the development literature.